As we enter 2025, the economic landscape continues to evolve, creating new challenges and opportunities for the housing market. Mortgage rates remain a key factor influencing affordability and buyer behavior, while broader economic trends hint at a more stable yet uncertain year ahead.

Mortgage Rates: Gradual Increases, Narrower Spreads

Mortgage rates have continued to edge higher, with the national average 30-year fixed rate once again crossing the 7% threshold. This marks a 1% increase since the Federal Reserve began cutting rates. However, there is a silver lining for homebuyers: the yield spread between mortgage rates and the 10-year U.S. Treasury yield has narrowed by approximately 0.15% over the past few months, bringing it closer to long-term historical averages. This narrowing spread has helped limit the impact of rising Treasury yields on mortgage rates.

For real estate agents, this means buyers may still face higher borrowing costs, but the rate environment is showing signs of stabilization. Communicating these trends to clients can help set realistic expectations and guide them through financing options.

Economic Trends: A Softer Landing Ahead?

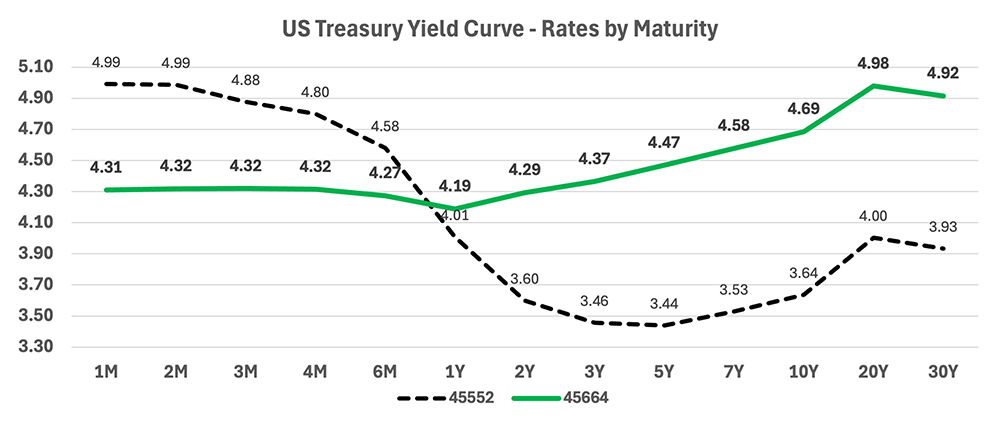

The U.S. Treasury yield curve has returned to an upward slope, a key indicator of economic stability. The market has largely priced in a “soft landing” scenario, where the economy slows but avoids a significant recession. Long-term Treasury yields remain attractive, with real returns of approximately 2.3%, assuming inflation remains contained.

For real estate professionals, this suggests a more predictable environment for mortgage rates, though uncertainty persists. Stable rates can provide a sense of security for buyers hesitant to enter the market amid volatility.

What to Expect in 2025

The prevailing outlook for 2025 is for generally stable mortgage rates, with only modest deviations higher or lower. Key factors that could influence rates include:

- Potential Headwinds: Stubborn inflation, large government deficits, and robust economic growth could push rates higher.

- Potential Tailwinds: A slowing economy, reduced inflation, or geopolitical uncertainty could bring rates down.

The Federal Reserve is expected to hold rates steady at its January 29 meeting, with only one or two rate cuts projected for the year. This would bring the Fed funds rate to 4%, aligning with a “normal” 10-year Treasury yield of around 5.5% and a 30-year mortgage rate near 7%.

Opportunities for Real Estate Agents

While higher rates may challenge affordability, this environment presents opportunities for agents to add value. Helping buyers navigate financing options—such as adjustable-rate mortgages (ARMs) or down payment assistance programs—can make homeownership more achievable. Additionally, a stabilizing rate environment could provide the predictability needed to reengage buyers who had paused their searches.